American health insurance seems to frustrate everyone. Patients complain that it’s expensive and complicated. Providers say it buries them in paperwork and can negatively affect patient care.

Poll after poll indicates that most people simply don’t trust their health insurance provider or the health care system itself. Fully 70 percent of the country thinks American health care has major problems or is in a state of crisis. Consumer satisfaction is at a 24-year low.

Frustration with health insurers may have turned to rage in a young man accused of killing a UnitedHealthcare executive in New York City on Dec. 4. The alleged killer appears to have been driven by an idea soon echoed on social media, that the woeful tale of American health care is a story with a villain, and the villain is health insurers.

Yet identifying a villain here is no simple matter.

The American health payment system is a ramshackle structure comprising public and private insurance plans offered by a host of providers across multiple states. Over many decades, the system has been layered with more legislative patches than the roof on your grandfather’s barn.

Despite the good intentions of lawmakers, regulators, countless health care workers, and insurance companies, health insurance remains expensive and confusing for the 92 percent of Americans who have it and for the 8 percent who don’t.

Despite its problems, many experts believe the health payment system can be improved. Some want to level the ground and build a new system from scratch. Others advocate refinements to make health insurance less expensive and more transparent. Any solution will require cooperation among a host of key players, including insurance companies, health care providers, state governments, and that most unpredictable of all institutions, the United States Congress.

Here’s an overview of the symptoms affecting the health care payment industry, some root causes, and cures suggested by industry analysts.

But first, here are the primary ways people get health insurance in the United States.

The Payers

Employer-sponsored insurance (ESI) is the most common way Americans get health care coverage. This includes self-funded plans, in which the employer acts as the insurer, and commercial health insurance purchased by a company for its employees. More than 178 million people had ESI in 2023, according to the U.S. Census Bureau.

Self-purchased health insurance is obtained by individuals directly from an insurance company, sometimes with the aid of an insurance agent or through the Affordable Care Act (ACA) Marketplace. The Marketplace offers premium discounts in the form of tax credits based on the buyer’s income. Nearly 34 million people bought their own health insurance in 2023. Of those, about 13.3 million used the Marketplace.

Medicare is a federal entitlement program that provides health insurance for Americans age 65 and above, people with a disability, and those having end-stage renal disease or ALS. Medicare covered about 63 million people in 2023.

Medicaid is a government program that provides health insurance and other benefits to low-income Americans. Medicaid is funded by both the federal government and the states. It is administered by the states within guidelines provided by the federal government. Coverage can vary from state to state. Medicaid covered about 63 million people in 2023.

Also in 2023, about 9 million people were covered by TRICARE, a program for U.S. servicemembers, their dependents, and retirees administered by the U.S. Department of Defense. Another 3 million people were covered by the Veterans Administration and related programs.

About 26 million people had no health insurance in 2023.

Symptoms

The most frequent complaint about health insurance is the cost. About half of Marketplace (55 percent) and ESI users (46 percent) gave their health insurance a negative rating based on its premiums in a 2023 survey by KFF. That’s roughly double the dissatisfaction rate for Medicare (27 percent) and Medicaid beneficiaries (10 percent).

The cost of ESI for a hypothetical family of four in 2024 was $32,066, according to the actuarial firm Milliman. Of that total, about 58 percent would typically be paid by the employer.

Cost is a major complaint for employers too, according to Orriel Richardson, an executive director at Morgan Health, a business unit of JPMorgan Chase aimed at improving health care.

“The growing refrain within small and mid-sized businesses is that providing health insurance for their employees is becoming unsustainable,” Richardson told The Epoch Times.

Another pain point with health insurance is the complexity of the plans. Consumers say this makes their coverage difficult to use and often seems unfair. Providers say the requirements are burdensome to them and make it more difficult to provide good health care.

Nearly two-thirds of Americans, 65 percent, said they don’t think health insurance providers are transparent about their coverage, according to a 2024 poll conducted by physician network MDVIP and Ipsos. Nearly the same number, 62 percent, find aspects of their health plan like co-insurance payments and deductibles hard to understand.

A 2023 KFF report showed that most people, 58 percent, had trouble using their insurance within the preceding year. Denied claims, provider network issues, and pre-authorization were commonly cited problems. About half of those who experienced problems were unable to find a satisfactory resolution.

Insurance companies generally do not publish their claim denial rates, though the data analysis firm Experian Health reported in 2024 based on provider surveys that claim denials are increasing. Thirty-eight percent of respondents said at least 10 percent of their claims were denied by the insurer. Some reported denial rates above 15 percent.

In 2021, just 0.2 percent of in-network denied claims were appealed by Marketplace enrollees, according to an analysis by KFF. The appeals were unsuccessful 59 percent of the time.

Providers are frustrated too. The administrative demands required by insurance companies are a particular pain point. Experian found that 65 percent of providers said meeting the insurers’ claim-submission requirements is harder now than before the pandemic.

More than 80 percent of nurses said the administrative demands imposed by insurance companies delay patient care, and about 75 percent said insurance policies reduce the quality of care according to a 2023 survey by the American Hospital Association. More than 80 percent of physicians said insurance policies hamper their ability to practice medicine.

Insurance companies are aware of the problems.

Andrew Witty, CEO of UnitedHealth Group, said as much in an op-ed in The New York Times just days after one of his executives was gunned down in New York.

“We know the health system does not work as well as it should, and we understand people’s frustrations with it. No one would design a system like the one we have. And no one did. It’s a patchwork built over decades,” Witty wrote on Dec. 13.

Causes

Witty touched on a root problem commonly mentioned by health insurance experts. The industry did not develop purely as a market response to a need as many other businesses did. It was patched together over a hundred years or so through a combination of business and government interventions.

“We are working with a healthcare system that was never truly designed for the purpose of making people healthier and having them live their optimal lives. It was always reactive to different things,” Richardson told attendees at a 2023 event sponsored by the Alliance for Health Policy.

ESI was started in the early 1900s by employers looking to ensure a reliable workforce. The Affordable Care Act now makes ESI mandatory for many employers. Medicare and Medicaid were created in 1965 to provide health coverage for uninsured Americans, though coverage has widened over time to provide access for more people.

The Employee Retirement and Income Security Act of 1974 was created to regulate employee pensions and includes a provision prohibiting states from regulating ESI plans, according to KFF. The Emergency Medical Treatment and Labor Act was added in 1986 to impose minimum standards for emergency care on hospitals accepting Medicare patients. COBRA, HIPAA, the Affordable Care Act, and the No Surprises Act also impose conditions on health insurance and medical services providers.

The many silos and layers of legislation make for a complex system that is difficult for Congress, let alone consumers, to understand.

For example, Richardson said, “You just don’t have a sense of how one change in a Medicare program has consequences across the broader health care marketing ecosystem.”

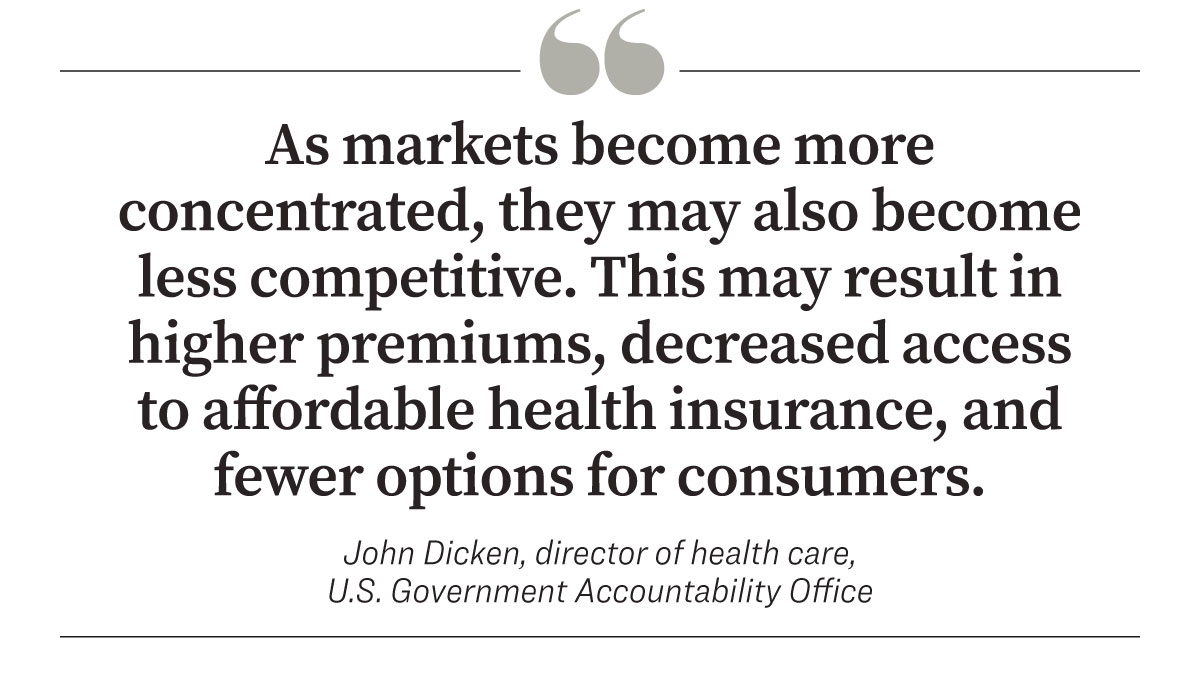

A second underlying condition affecting health insurance is consolidation. Private health insurance has become more concentrated among fewer, larger insurers and care providers. The six largest health insurers in the country accounted for nearly 30 percent of all U.S. health care spending in 2023, according to an analysis conducted by Axios. That’s up from less than 10 percent in 2011.

“As markets become more concentrated, they may also become less competitive. This may result in higher premiums, decreased access to affordable health insurance, and fewer options for consumers,” John Dicken, director of health care at the U.S. Government Accountability Office wrote in a Dec. 5 article.

A state’s insurance market is concentrated when fewer than four insurance companies control 80 percent or more of the market share. Some 95 percent of U.S. health insurance markets in metropolitan areas were highly concentrated in 2022, according to the American Medical Association. In nearly half of those areas, a single health insurer controlled at least 50 percent of the market.

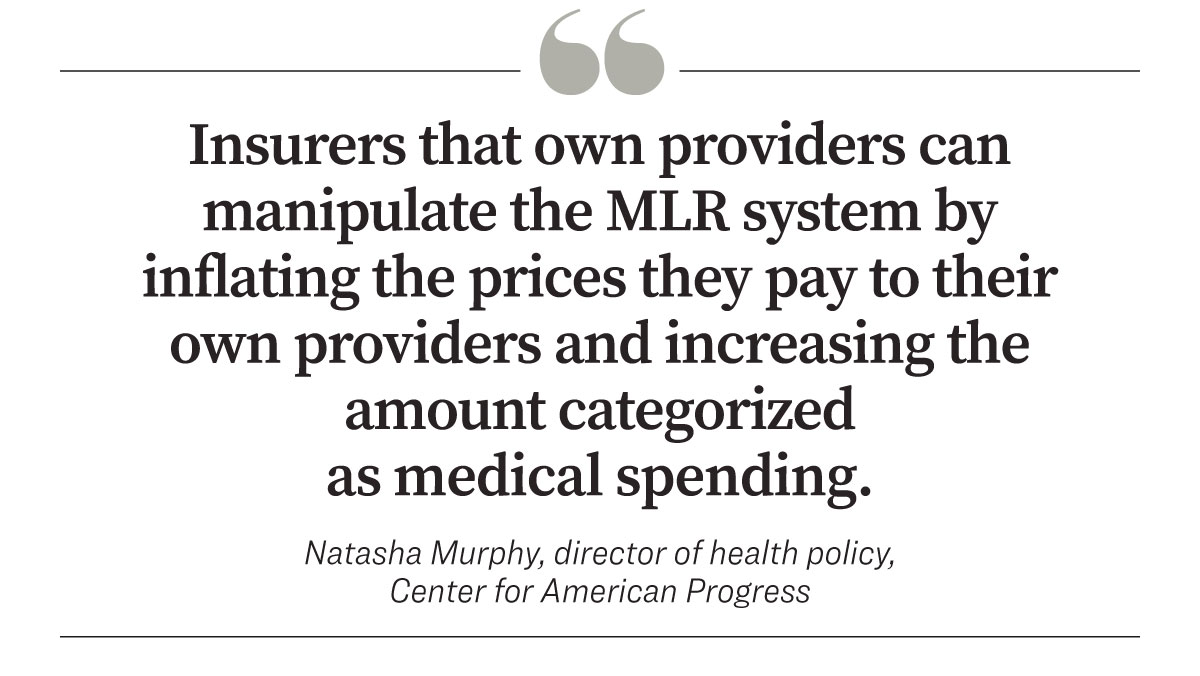

Insurers have also consolidated vertically, meaning that some have acquired the health providers they pay for services. This can make it harder for the government or consumers to track how much of the money paid in insurance premiums is actually spent on health care.

That number, known as the medical loss ratio (MLR), is a key metric in both public and private health insurance. When the MLR dips below a certain threshold—typically 80 or 85 percent depending on the type of insurance—the company is required to rebate premiums to the consumer.

“Insurers that own providers can manipulate the MLR system by inflating the prices they pay to their own providers and increasing the amount categorized as medical spending,” Natasha Murphy, director of health policy for the Center for American Progress, a progressive policy institute, wrote in a December 2024 report.

The argument in favor of consolidation is that it helps insurers reduce rates by gaining efficiency and negotiating better rates from health care providers. Some surveys have shown that physicians who work in integrated health systems have higher rates of job satisfaction.

Perhaps the most sobering root problem affecting the cost of health insurance is that Americans, on the whole, are sicker than they used to be.

Millennials are significantly less healthy than their Generation X predecessors, according to a 2019 study conducted by the Blue Cross Blue Shield Association.

The study found that about one-third of Millennials suffer from conditions that can affect quality of life and reduce life expectancy. Millennials had higher rates of cardiovascular disease and endocrine conditions such as diabetes.

Dr. Arthur Agatston, writing in a journal of the American Heart Association, concluded that Americans face an obesity crisis. The reason they are “fatter and hungrier and sicker,” according to Agatston, is due to their lifestyle. “The answer is too much fast, processed food, too little exercise, and too little sleep,” he wrote.

Life expectancy in the United States dropped by 2.7 years from 2019 to 2021, according to the Centers for Disease Control and Prevention, reaching its lowest level since 1996. Over the same period, the U.S. population grew by nearly 2.7 million.

“Health care is just simply not working. We’re sicker, our life expectancy is lower, our quality of life is poor,” Richardson said.

All of that impacts the cost of health insurance, as it costs more to provide health care to a larger, sicker population.

Prescriptions for Change

Ideas for improving the health payment system come in two types: reboots and refinements.

Reboots include ideas for sweeping change, such as the Medicare for All proposal advocated by Sen. Bernie Sanders (I-Vt.). The proposal would create a national health insurance program to provide comprehensive health care for all U.S. residents.

Liran Einav of Stanford University and Amy Finkelstein of the Massachusetts Institute of Technology have proposed a narrower version of universal health coverage. Under their proposal, all Americans would automatically be enrolled in basic health coverage at no cost to the enrollee. People could supplement that coverage with self-paid private insurance if they chose to.

Unlike Medicare and Medicaid, which have no cost cap, the Einav-Finklestein plan would set an overall limit on taxpayer spending for health care.

Other ideas for improving health insurance would maintain the basic framework of public and private insurance systems but refine it to reduce cost and improve transparency. Several of these ideas focus on making health insurance more competitive.

Bruce Ratner, a former head of the Consumer Protection Division for New York City, advocates requiring health insurers to publish their denial rates. That would likely require an act of Congress and would lower prices according to Ratner.

“That way we choose our company based on denial rates, and that makes the companies work very hard to be competitive,” Ratner said in a Dec. 9 interview with CNBC.

Mark Bertolini, CEO of Oscar Health, advocates eliminating ESI to improve competition. Oscar Health is an insurance company that uses data to match individuals with tailored health coverage.

“The ability of your employer to negotiate against the large insurance company that has much a larger relationship with the provider community is very stunted now,” Bertolini said in a Dec. 13 interview with CNBC.

Small and mid-sized companies are hit hardest, seeing double-digit annual rate increases for their health plans, Bertolini said. That’s because they must buy more expensive plans to meet the needs of all employees. Giving employees a cash contribution for health insurance rather than purchasing a plan for them would allow each person to select the insurance that fits their needs, Bertolini said.

Competition could be increased also by eliminating anti-competitive contracting practices used by some large insurance companies and health care providers, according to Nicole Rapfogel and Marquisha Johns of the Center for American Progress.

Those practices include clauses that force a provider to charge an insurer lower rates than those offered to other companies, gag clauses that prevent either the payer or provider from disclosing price information to patients, and exclusivity clauses that make the contracted provider the only in-network option.

Improving the transparency in the industry would also improve the situation, according to Richardson.

Health insurers operate in multiple states, often offering a mix of individual, ESI, Medicare Advantage, and other plans, each with its own standards and definition. That makes it difficult for anyone to assess the entire industry and has given rise to a multi-billion-dollar industry around health care data, said Richardson.

One solution might be “a real transparency report that says, if a new Medicare requirement comes onboard, how do you show that effect was isolated within that Medicare book of business and not … a ripple effect went into the other books of business,” she said.

Insurers are quick to point out that their sometimes confusing rules are intended to reduce costs by preventing wasteful or fraudulent use of the health care system. Many people are skeptical of that.

Insurers could help by educating customers on how insurance works and the reasons behind their coverage decisions, according to Witty.

“Together with employers, governments, and others who pay for care, we need to improve how we explain what insurance covers and how decisions are made,” he said. “Behind each decision lies a comprehensive and continually updated body of clinical evidence focused on achieving the best health outcomes and ensuring patient safety.”

Acknowledging the growing urgency to improve health insurance, Richardson likens the system to a house with several layers of shingles on the roof. At some point, previous solutions may need to be peeled away to ensure that the system survives.

“We have a house that is sustainable enough, but instead of removing the shingles to repair the roof we keep cobbling new shingles onto it,” she said. “The very house itself is going to collapse under this patchwork of things we keep doing.”